Los próximos seis meses parecen prometedores en la industria de ventas de aviación. La Asociación Internacional de Distribuidores de aeronaves (ya) predice un mercado normalizado para los próximos seis meses basado en 2022 ventas en el mercado. Siga leyendo para aprender más.

Los próximos seis meses parecen prometedores en la industria de ventas de aviación. La Asociación Internacional de Distribuidores de aeronaves (ya) predice un mercado normalizado para los próximos seis meses basado en 2022 ventas en el mercado. Siga leyendo para aprender más.

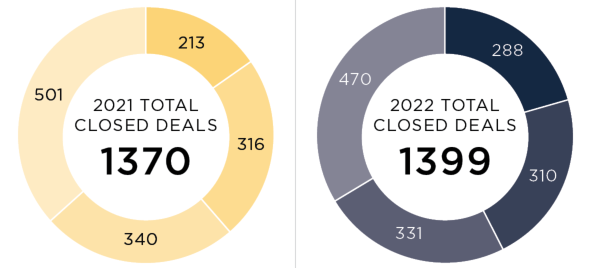

Si bien el volumen anual de reventa de aviones comerciales fue ligeramente superior para los miembros de la Asociación Internacional de Concesionarios de Aeronaves (ya) en 2022, Los concesionarios de aeronaves indican que las condiciones del mercado están normalizando. En el recientemente lanzado 2022 Informe del mercado de la IdaA del cuarto trimestre, Informaron concesionarios acreditados por IADA y corredores certificados 1,399 transacciones de ventas de aeronaves usadas cerradas en 2022, comparado con 1,370 en 2021, un aumento del dos por ciento, y el total más alto para los miembros de IADA en la memoria reciente.

Para el año acaba de terminar, Volumen de reventa representado $9.3 mil millones en ventas, o un promedio de aproximadamente $8 millones por transacción. Como se esperaba, Diciembre fue el mes más ocupado del año con 259 reventas informadas, Duplicar fácilmente el promedio de rendimiento mensual del año, y superando a diciembre de 2021 255 actas.

El mercado se dirigió hacia un mayor equilibrio

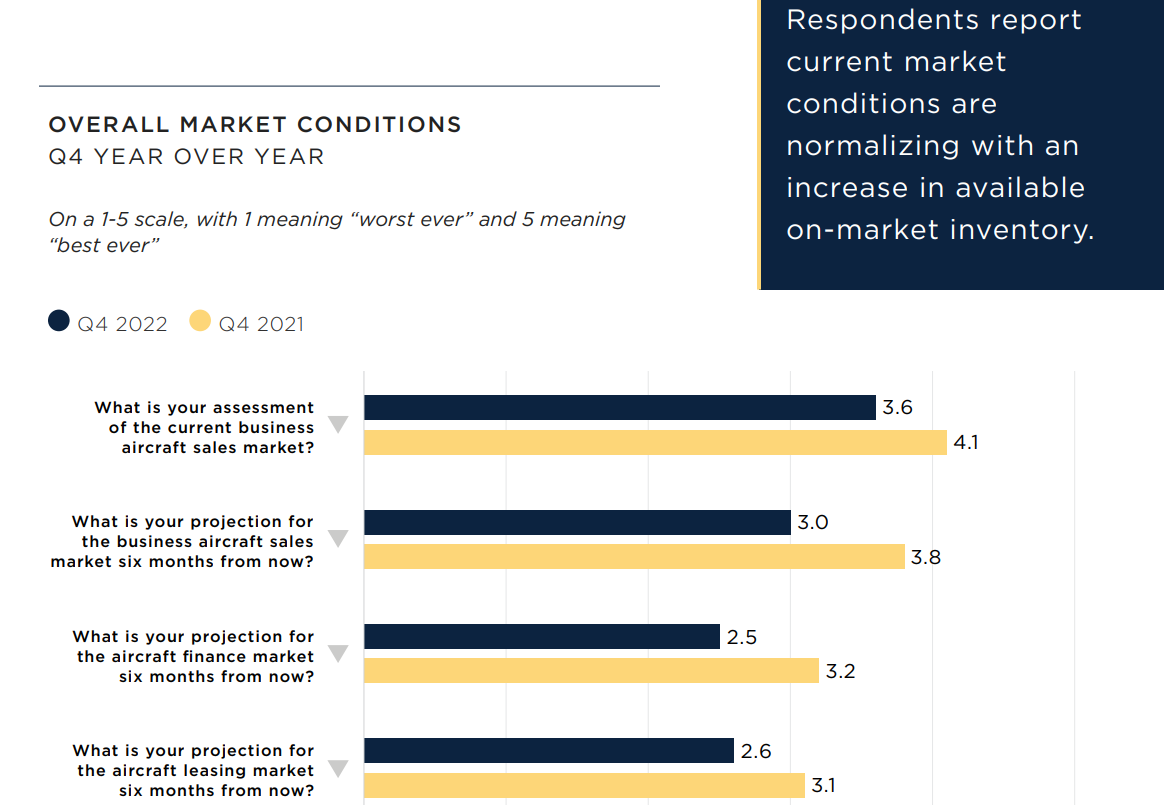

"Pensando en el futuro, Los miembros de la IADA tienen expectativas un poco más modestas que hace un año para el mercado de reventa de aviones en los próximos seis meses,ha elegido a David Monacell como presidente de la junta y a Zipporah Marmor como vicepresidenta. “Basado en nuestra encuesta de perspectiva de los miembros de la IADA, Las proyecciones de reventa de seis meses más moderadas también son ciertas para el mercado de finanzas de aviones y arrendamiento de aeronaves,"Starling agregó.

Basco de Austin, Gerente de investigación de mercado para el concesionario acreditado Ogarajets en Atlanta, dijo "En los próximos seis meses, Creo que continuaremos viendo la normalización del mercado. Anticipo un mercado más equilibrado, con la mayoría de las aeronaves que comienzan a depreciarse a niveles ligeramente más altos que los niveles previos a la pandemia,Bass agregado, "El precio de los aviones a la actualidad y heredado probablemente caerá el más, mientras que el precio de los aviones recién entregados probablemente se beneficiará de los atrasos OEM ”.

Datos cualitativos y cuantitativos en el informe de mercado

Las perspectivas y proyecciones de los miembros de IADA para el informe del mercado de IADA están informados por los informes de actividad mensuales presentados por los concesionarios IADA a través de AircraftExchange. Las perspectivas y proyecciones de los miembros de IADA para el Informe de mercado de IADA se basan en los informes de actividad mensuales presentados por los distribuidores acreditados de IADA a través de AircraftExchange., Las perspectivas y proyecciones de los miembros de IADA para el Informe de mercado de IADA se basan en los informes de actividad mensuales presentados por los distribuidores acreditados de IADA a través de AircraftExchange., Las perspectivas y proyecciones de los miembros de IADA para el Informe de mercado de IADA se basan en los informes de actividad mensuales presentados por los distribuidores acreditados de IADA a través de AircraftExchange.. Para registrarse para descargar el 2022 Informe del mercado del cuarto trimestre de la IADA ir a https://aircraftexchange.com/market-report.

Las perspectivas y proyecciones de los miembros de IADA para el informe del mercado de IADA están informados por los informes de actividad mensuales presentados por los concesionarios IADA a través de AircraftExchange. Las perspectivas y proyecciones de los miembros de IADA para el Informe de mercado de IADA se basan en los informes de actividad mensuales presentados por los distribuidores acreditados de IADA a través de AircraftExchange., Las perspectivas y proyecciones de los miembros de IADA para el Informe de mercado de IADA se basan en los informes de actividad mensuales presentados por los distribuidores acreditados de IADA a través de AircraftExchange., Las perspectivas y proyecciones de los miembros de IADA para el Informe de mercado de IADA se basan en los informes de actividad mensuales presentados por los distribuidores acreditados de IADA a través de AircraftExchange.. Para registrarse para descargar el 2022 Informe del mercado del cuarto trimestre de la IADA ir a https://aircraftexchange.com/market-report.

Los miembros de la IADA señalaron que los próximos seis meses deberían generar un ligero aumento en el inventario y las perspectivas estables para el suministro, voluntad de inventario y demanda. Esto es válido para todos los segmentos de aviones comerciales, incluyendo turbopropulsores, chorros de luz, jets medianos, y aviones comerciales de rango grande y ultra largo.

El año hasta la fecha, Miembros de la IADA informaron 688 Nuevos acuerdos de adquisición en 2022, 723 Retenido exclusivamente para vender acuerdos, 104 Transacciones de precios bajas, 85 ofertas que se desmoronaron, y 972 aviones bajo contrato. La actividad general fue similar a la de 2021, excepto que hubo más transacciones de precios bajas en 2022 y menos aviones bajo contrato.

Comentarios de los miembros de la IADA

“La demanda del mercado ha superado enormemente la oferta durante los últimos dos años y, aunque este sigue siendo el caso, La demanda extrema del mercado se ha resuelto recientemente después de los precios del mercado que se elevó a los máximos de todos los tiempos en el verano de 2022 resultando en la oferta y la demanda avanzando hacia la alineación ". — Vicepresidente de Iada Phil Winters, VP de ventas & Gestión de aeronaves/carta, Avión occidental, Idaho.

“Total, El mercado parece muy resistente y saludable por el momento. El lado de la demanda del mercado (compradores) continúa haciendo un buen trabajo absorbiendo la creciente cantidad de inventario que golpea el mercado. Esto sigue sorprendiéndome, Aunque tal vez ya no debería.” –Shawn Dinning, Socio principal en Dallas Jet International, Texas.

“Continuamos experimentando una demanda de clientes muy fuerte. La mitad de nuestras transacciones están en aviones que nunca ven el mercado abierto y 100 El porcentaje de esas transacciones actuales fuera del mercado incluye un concesionario/corredor de IADA en el otro lado.” — Jim Riner, Dueño / Director general, Aviación de Wetzel, Colorado.

“Mientras que los inventarios se elevaron ligeramente sobre el Q3/Q4, Ogara rastreó cuatro semanas consecutivas en diciembre. Nuestra tubería Q1 permanece al ras de un puñado de transacciones "sobrantes" ‘22, así como varios listados y compromisos de adquisición nuevos. El mercado actual todavía favorece al vendedor; sin embargo, Esperamos ver una lenta construcción de suministro a medida que avanzamos en el segundo trimestre y el verano., Creando un poco de ablandamiento en los precios. dicho esto, No predecimos un edificio significativo de la oferta ni una dilución significativa de los precios.” — Johnny Foster, Presidente & CEO, en Ogarajets, Georgia.

¿Quién hubiera pensado que un avión comprado nuevo a un OEM hace menos de tres años puede venderse en el mercado actual con una prima en comparación con lo que pagó el propietario por él?. Cubre las percepciones de los distribuidores acreditados por la IADA sobre el mercado tomado de su encuesta de miembros de la IADA, ¿Quién hubiera pensado que un avión comprado nuevo a un OEM hace menos de tres años puede venderse en el mercado actual con una prima en comparación con lo que pagó el propietario por él?, Incluso cuando el inventario es difícil de ubicar y puede que nunca aparezca en el mercado abierto. Sin embargo, No incluye transacciones de aeronaves previas realizadas únicamente por los miembros OEM de IADA.

¿Quién hubiera pensado que un avión comprado nuevo a un OEM hace menos de tres años puede venderse en el mercado actual con una prima en comparación con lo que pagó el propietario por él?. Cubre las percepciones de los distribuidores acreditados por la IADA sobre el mercado tomado de su encuesta de miembros de la IADA, ¿Quién hubiera pensado que un avión comprado nuevo a un OEM hace menos de tres años puede venderse en el mercado actual con una prima en comparación con lo que pagó el propietario por él?, Incluso cuando el inventario es difícil de ubicar y puede que nunca aparezca en el mercado abierto. Sin embargo, No incluye transacciones de aeronaves previas realizadas únicamente por los miembros OEM de IADA.